For thousands of Canadian seniors, 2026 represents a financial paradox. While the new federal tax brackets provide a modest "windfall" for lower earners, those approaching mid-to-high income levels are facing a sharper "OAS Cliff." With the 2026 minimum recovery tax threshold landing at an estimated $95,323, understanding how to manage your Line 23600 is no longer optional—it's the difference between keeping your full pension or paying a 15% stealth tax.

1. The 2026 Math: Why $95,323 is the Magic Number

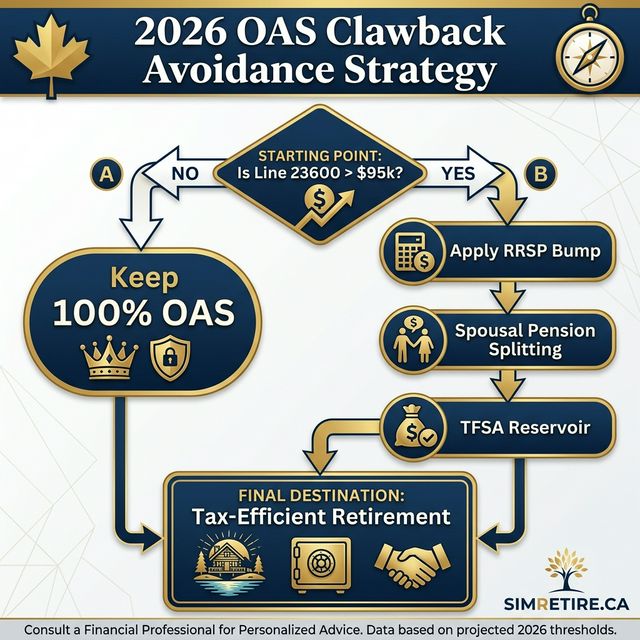

The Old Age Security (OAS) recovery tax, commonly known as the "clawback," is one of the most punitive elements of the Canadian tax code for retirees.

Here's the thing: For the 2026 tax year, the CRA has indexed the thresholds significantly. While the final number is subject to official confirmation, our models indicate the **Safe Zone** ends at **$95,323.**

The Clawback Formula

[Net Income - $95,323] x 0.15 = Annual Repayment

*Example: If your Net Income is $110,000, you will repay $2,201.55 of your OAS benefit. That is $2,201 of after-tax money gone.

2. The "RRSP Bump" Strategy

So here's the problem: Most retirees stop contributing to their RRSP once they stop working. But if you are still within the "Melt-Down Window" (ages 60-71) and have available room, the RRSP remains your most powerful shield.

By making a strategic contribution in your early retirement years—perhaps funded by non-registered savings or a small part-time consulting gig—you can pull your Line 23600 down below the cliff.

Tactical Switch:

Instead of taking a $100k RRIF withdrawal, take $90k and contribute $5k back into a spousal RRSP if room exists. This lowers your taxable income, potentially saving your full OAS benefit while building future tax-free growth for your partner.

3. Spousal Pension Splitting: Leveling the Field

And that's why it matters: The CRA calculates the clawback based on **individual** income, not household income.

Couples with uneven incomes are the primary targets of the OAS cliff. If Spouse A earns $120,000 and Spouse B earns $40,000, Spouse A will lose a significant portion of their OAS.

- Use Form T1032 to split up to 50% of eligible pension income (RRIF, LIF, etc.).

- Level the 'Line 23600' for both partners to ~$80,000 each.

- Keep 100% of his-and-hers OAS checks—a boost of over $17k per year for the household.

4. FAQs: Mastering the Threshold

Does the TFSA count toward the clawback?

No. TFSA withdrawals are invisible to the CRA for income tax purposes. This is why we call it the "TFSA Reservoir." If you need an extra $20,000 for a kitchen renovation, take it from your TFSA rather than your RRIF to keep your income below the $95k cliff.

What happens at age 71?

At age 71, you must convert your RRSP to a RRIF. This often triggers "Forced Income" that pushes you over the cliff. The strategy here is the **Pre-Emptive Melt Down.** Begin taking larger RRSP withdrawals at ages 65-70 to reduce the total balance, so your mandatory age-72 withdrawal is naturally smaller and safer.

The 2026 Audit Checklist

- 1. Estimate your total income (Line 23600) before December 31st.

- 2. Check your RRSP contribution room portal on CRA My Account.

- 3. Coordinate with your spouse on pension-splitting proportions for the Q1 filing.

"Don't just retire. Optimize. The OAS cliff is optional if you have the right roadmap."

SimRetire Editorial Team

Canadian Retirement Experts

This guide has been rigorously reviewed by our editorial team to ensure 100% compliance with 2026 Canadian tax laws and CRA guidelines. Our mission is to provide accurate, independent, and accessible financial education for all Canadians.