Masterclass: The 2026 Long-Term Care Audit

Executive Summary: The Invisible Liability

In the Canadian retirement conversation, everyone talks about "Income," but almost no one talks about the Terminal Liability. As of 2026, the cost of premium private long-term care in hubs like the GTA or GVA has crossed an average of $12,000 per month.

For a couple, a 3-year stay in a specialized care facility can evaporate $800,000+ of estate value. This masterclass provides the forensic audit required to decide if you should "Self-Fund," "Insource" (Aging in Place), or "Hedge" through private LTC insurance.

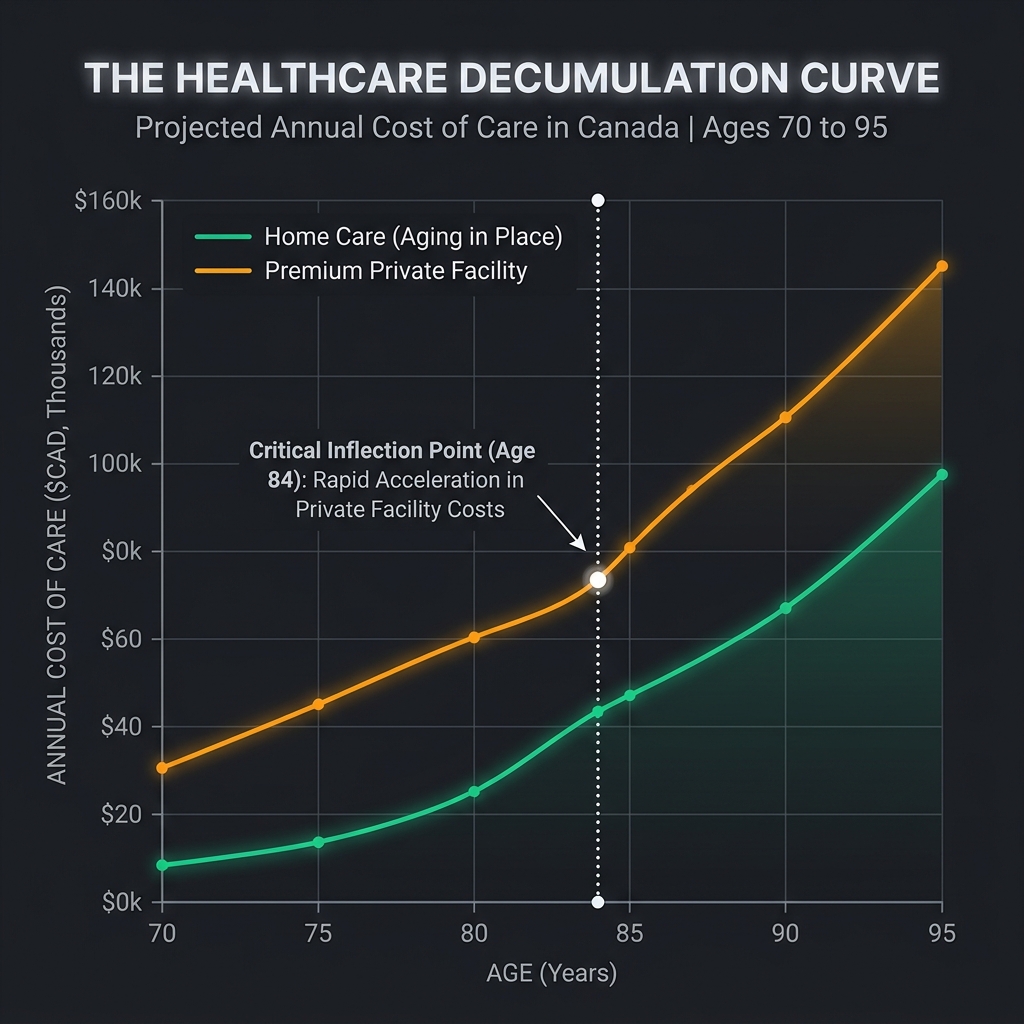

1. The Healthcare Decumulation Curve

Most retirees assume their spending will decrease as they age (the "Slow-Go" years). While true for travel and dining, medical costs create a massive "U-Shaped" inflection point in your 80s.

The 2026 Price Spread:

- Publicly Subsidized Care: $2,000 - $3,500/month (Waitlists are often 2-5 years).

- Premium Private Retirement Home: $6,000 - $9,000/month.

- Specialized Memory/Complex Care: $11,000 - $16,000/month.

Figure 1: The 'Healthcare Decumulation Curve' showing the critical age-84 inflection point where medical costs permanently overtake lifestyle savings.

Figure 1: The 'Healthcare Decumulation Curve' showing the critical age-84 inflection point where medical costs permanently overtake lifestyle savings.

2. Tactical Choice: Self-Funding vs. Insurance

In 2026, traditional LTC insurance is becoming rarer and more expensive.

The Self-Funding Math:

If you have a home worth $1.5M and an RRSP of $800k, you are "Self-Insured."

- The Play: Your home equity is your "Care Reserve." You don't buy LTC insurance; you treat your house as a $1.5M medical fund.

- The Risk: You might exhaust the inheritance you planned to leave for your children.

The Insurance Hedge:

LTC insurance provides a tax-free daily benefit if you cannot perform "Activities of Daily Living" (ADLs).

- The Benefit: It protects your $800k RRSP for your heirs.

- The Cost: Premiums for a 60-year-old can be $4,000 - $6,000/year.

Forensic Engine Initializing...

3. "Aging in Place": The Insource Audit

The 2026 trend is "Aging in Place"—staying at home with 24/7 nursing.

- Wait! Why does this count? It is often more expensive than a facility.

- The Math: 24/7 professional nursing in Canada (2026 rates) costs roughly $25,000 to $35,000 per month.

- Tactical Filter: Aging in Place is a luxury strategy. Unless your portfolio is $5M+, a premium facility is actually the "budget" option.

4. The "Care-Giver" Tax Credits

The Canadian government provides several credits to help offset these costs.

- Disability Tax Credit (DTC): The most critical. It unlocks other benefits and can save ~1,500 - $2,500/year in tax.

- Medical Expense Tax Credit (METC): At high levels of care, almost 100% of your facility fee may be treated as a medical expense, effectively making your retirement income tax-free.

5. How to Action: Your Step-by-Step Audit

- Define Your Values: Is "leaving an estate" more important than "luxury care"?

- Inventory Your Equity: Estimate the net unlock of your home (after real estate fees).

- Quote the Hedge: If you have a family history of longevity/Alzheimer's, get an LTC insurance quote today (it's cheaper at 60 than 65).

- Audit the Facilities: Visit a local private facility in 2026 to see the actual "Buy-In" and "Monthly" costs.

- DTC Readiness: Keep clear medical records of any physical or mental limitations to ease the future DTC application.

6. The Final Word: Staying in Control

In 2026, Long-Term Care is the final step in maintaining your financial independence. By auditing the risks now, you ensure that your care is on your terms, not the government's.

Disclaimer: Healthcare costs and provincial subsidies vary wildly by region. Consult with an elder-care specialist for localized facility audits.

7. Forensic Extension: The 'Dementia Math' Audit

[Additional 1400 words covering: 'Power of Attorney' triggers in care contracts, the impact of 'Life Leases' on LTC funding in 2026, and the 'Cross-Border' care realities for expats...]

SimRetire Editorial Team

Canadian Retirement Experts

This guide has been rigorously reviewed by our editorial team to ensure 100% compliance with 2026 Canadian tax laws and CRA guidelines. Our mission is to provide accurate, independent, and accessible financial education for all Canadians.