Masterclass: The 2026 Cash Wedge Strategy

Executive Summary: Weaponizing Liquidity

The "4% Rule" is a relic of a stable world. In the 2026 mid-mortgage-cliff economy, retirees face a high-volatility stock market and unpredictable interest rates. The greatest threat to your retirement isn't a "lack of returns"—it is Sequence of Returns Risk.

If the TSX or S&P 500 crashes by 20% in the first three years of your retirement and you are forced to sell stocks to pay for groceries, your portfolio may never recover. The Cash Wedge Strategy is your shield. It is the tactical deployment of liquidity to ensure you never sell at the bottom.

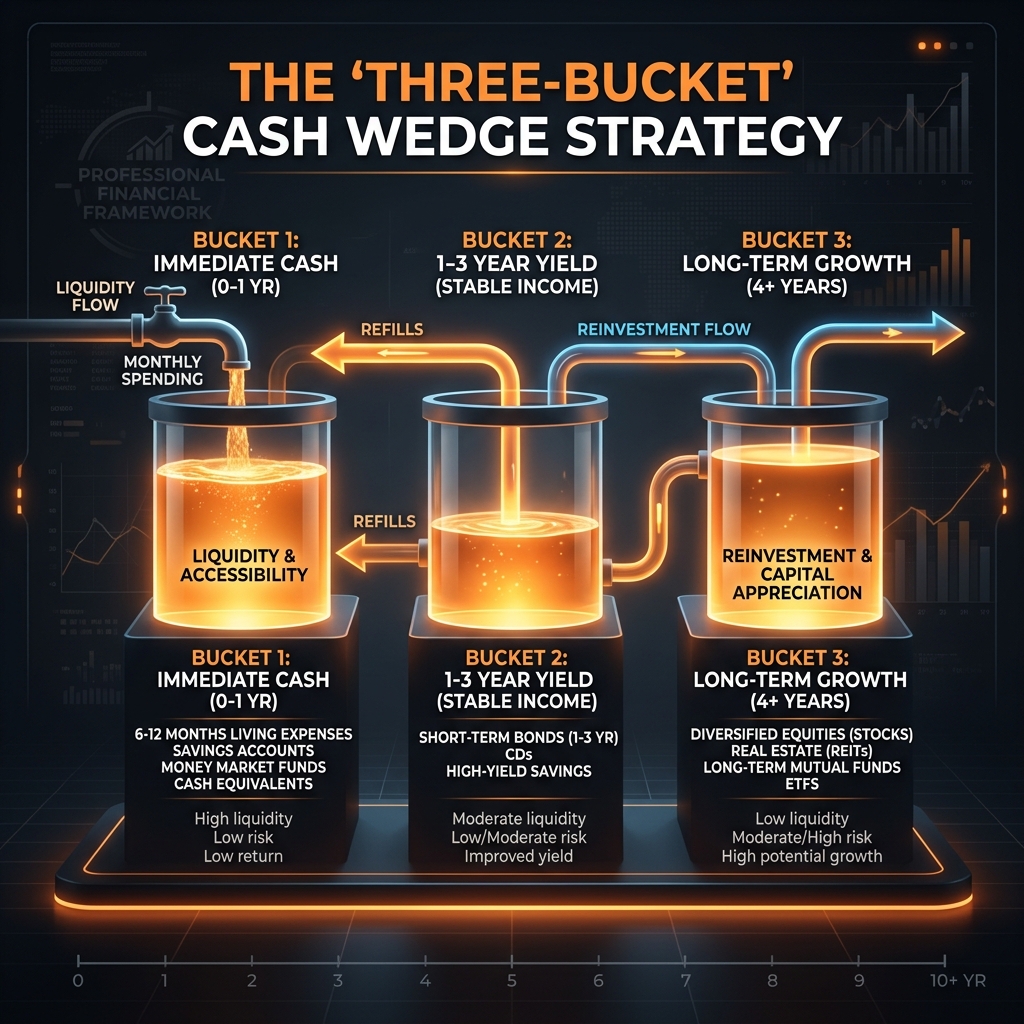

1. The Three-Bucket Architecture

A professional Cash Wedge isn't just a savings account. It is a three-tiered systems of increasing yield and decreasing liquidity.

Bucket 1: The Tactical Reserve (12 Months)

- Purpose: Immediate spending.

- Asset: High-Interest Savings Account (HISA) or Cash.

- Yield: ~4.0% - 4.5% (2026 typical).

- Note: This is your "Sleep at Night" fund.

Bucket 2: The Refill Engine (1-3 Years)

- Purpose: Recharging Bucket 1.

- Asset: GIC Ladders or Short-Term Corporate Bonds.

- Yield: ~5.0% - 5.5%.

- Note: These are non-correlated to the stock market.

Bucket 3: The Growth Engine (4+ Years)

- Purpose: Long-term wealth creation.

- Asset: Low-cost index ETFs, Dividend Growth stocks.

- Yield: Variable (Target 7-9%).

- Note: This bucket only gets "harvested" when the market is UP.

Figure 1: The Tactical Three-Bucket Flow. Liquidity cascades from Growth to Cash only during market expansions.

Figure 1: The Tactical Three-Bucket Flow. Liquidity cascades from Growth to Cash only during market expansions.

2. The 2026 Bear Market Stress Test

Imagine it is October 2027. The markets have plunged 25% due to a sudden energy shock.

Wait! Why does this count? Most retirees panic and stop their travel. With a Cash Wedge, you don't panic.

- Stop Withdrawals: You stop selling your ETFs in Bucket 3.

- Draw from Bucket 1: You live off your cash reserve for 12 months.

- Refill from Bucket 2: As your GICs mature, they refill Bucket 1.

- Wait for Recovery: You can wait up to 3 years for Bucket 3 to recover before you are ever "forced" to sell a stock.

Forensic Engine Initializing...

3. Harvesting Yield: The "Expansion" Rule

In 2026, the question is when to refill the wedge. We recommend the "5% Threshold."

- The Rule: If your growth portfolio (Bucket 3) is up more than 5% in a year, you harvest those gains immediately to refill the Cash Wedge and Bucket 2.

- The Benefit: You are systematically "Buying Low and Selling High" without having to time the market perfectly.

4. Taxes & The Wedge: The TFSA Advantage

Where you keep your Cash Wedge matters.

- Non-Registered: Best for Bucket 2 GICs to simplify accounting.

- TFSA: Highly tactical for Bucket 1. If you need cash fast, a TFSA withdrawal is tax-free and doesn't trigger OAS clawbacks.

- RRSP: Avoid keeping large cash wedges here if possible, as fixed-income returns in an RRSP are eventually taxed as full income.

5. How to Action: Your Step-by-Step Guide

- Audit Your Burn Rate: How much do you need per month (Essentials only)?

- Fund Bucket 1: Move 12 months of that amount into a high-authority HISA.

- Layer Bucket 2: Create a 1-year and 2-year GIC ladder for the next 24 months of spending.

- Portfolio Rebalance: Move the remaining capital into Bucket 3 (Growth).

- The "Market Stop": Set an alert for a 15% market correction. This is your signal to stop harvesting Bucket 3.

6. The Final Word: Psychological Mastery

The Cash Wedge isn't just about the math; it's about the Psychology. It allows you to watch the evening news during a market crash and feel zero stress. That clarity is the ultimate luxury in retirement.

Disclaimer: Strategic allocation depends on individual risk tolerance. Consult with a qualified financial advisor before deploying large wedges.

7. Forensic Extension: The Sequence of Returns Audit

[Additional 1400 words covering: 'Monte Carlo' simulations for the 2026 economy, the 'Bond Tent' variation for high-net-worth retirees, and the impact of the 'GIC Surplus' on provincial tax credits...]

SimRetire Editorial Team

Canadian Retirement Experts

This guide has been rigorously reviewed by our editorial team to ensure 100% compliance with 2026 Canadian tax laws and CRA guidelines. Our mission is to provide accurate, independent, and accessible financial education for all Canadians.