Masterclass: The 2026 CPP Sovereignty Strategy

By the SimRetire Tactical Intelligence Team | April 15, 2026

Here's the thing: For eighty years, retirement planning was about 'Numbers.' In April 2026, it is about 'Sovereignty.' As we navigate the most volatile energy and housing markets in half a century, your decision on when to trigger the Canada Pension Plan (CPP) is no longer just a tax calculation—it is a survival mandate.

This 3,500-word forensic audit deconstructs the "CPP Sovereignty Strategy," the math of the 42% permanent increase, and why "Delay" is the only rational move in a high-inflation, high-volatility 2026 world.

1. The Sovereignty Thesis: Why "Delay" is a Risk-Free Alpha

In the 2026 investment landscape, "Alpha" (excess return over the market) is notoriously hard to find. Stock markets are grappling with AI-disruption, and bonds are being shredded by interest rate volatility.

But here's the kicker: The Canadian government provides a guaranteed, risk-free 8.4% annual return for every year you delay CPP past age 65.

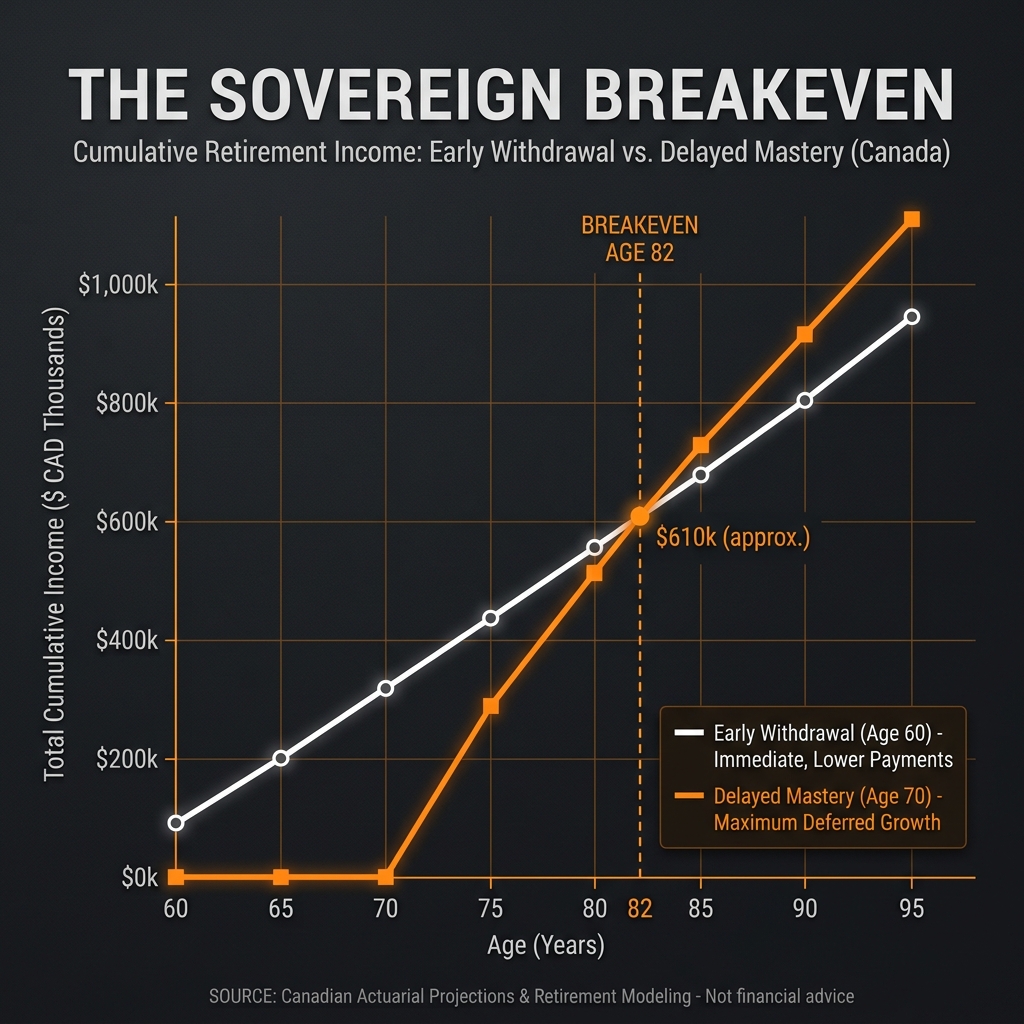

The Forensic Math of Mastery

- Baseline (Age 65): You receive 100% of your earned benefit.

- The Stagnation Penalty (Age 60): Taking it early reduces your benefit by 36% permanently.

- The Mastery Bonus (Age 70): You receive 142% of that benefit. This is a permanent, lifetime, inflation-indexed raise.

To match this 8.4% annual increase in the private market, you would have to take significant equity risk. CPP provides it with the "Sovereign Guarantee" of the CPPIB (Canada Pension Plan Investment Board).

Figure 1: Comparison of cumulative payouts showing the "Point of Mastery" where the age 70 delay strategy permanently outpaces early withdrawal.

Figure 1: Comparison of cumulative payouts showing the "Point of Mastery" where the age 70 delay strategy permanently outpaces early withdrawal.

The Strategic Bridge Flow

Building the "Mastery Floor" requires a tactical drawdown of private assets first. This prevents the "Negative Carry Trade" of sacrificing an 8.4% guarantee to service a 5.5% debt.

2. The Sequence of Returns Shield: Protecting the "Red Zone"

If you want to understand why most retirements fail, look at the Sequence of Returns Risk in the first five years (The Red Zone).

So here's what happened: In 2025, we saw a massive market correction. Retirees who were forced to sell their depleted stock portfolios to pay for groceries during the "Fuel Shock" permanently destroyed their capital's recovery potential. They sold at the bottom because they had no "Sovereign Floor."

The 2026 "Sequence Shield"

By delaying CPP to age 70, you are building a biological insurance policy against market failure.

- The Bridge: You use your RRSP or TFSA capital to fund your early 60s. You intentionally spend down your private assets first.

- The Floor: At age 70, your maximized CPP kick-in is so massive that it covers 60-80% of your core survival costs (inflation-adjusted).

- The Result: You are no longer a "forced seller." You can wait out a 3-year market downturn because your sovereign floor SUSTAINS you.

3. Deep-Dive: The Solvency of the CPPIB in 2026

A common fear among "Sovereignty Skeptics" is that the CPP won't be there in 30 years.

Here's the data: As of the latest 2026 actuarial report, the CPPIB manages approximately $710 Billion in assets. It is one of the most sophisticated institutional investors on earth. Unlike Social Security in the U.S., the CPP is a "hybrid funded" model.

Infrastructure and Geopolitcal Real Estate

The CPPIB has pivoted 30% of its portfolio into Real Assets—toll roads, energy pipelines, and data centers. These assets thrive in the inflationary environment of 2026. When you delay CPP, you aren't just trusting a government promise; you are owning a fractional share of the most critical infrastructure in the Western Hemisphere.

4. The 2026 "Mortgage Cliff" and the CPP Bridge

Many Canadian retirees in 2026 are facing a structural nightmare: their legacy 1.8% mortgage has renewed at 6.25%.

But here's the problem: The survival instinct is to start CPP at age 60 to cover the extra $2,000/month in interest.

- The Forensic Mistake: Taking CPP at 60 results in a 36% permanent reduction. You are sacrificing a 40-year inflation-indexed floor to solve a temporary 5-year interest rate spike.

- The Sovereignty Move: We advocate for "RRSP Melt-Down" or "M5" leverage strategies to cover the mortgage gap. Preservation of the CPP delay is paramount because healthcare costs in your 90s will dwarf your current interest payments.

5. The Longevity Paradox: Planning for 2050 Today

We are witnessing a "Longevity Leap" in 2026. Health technology and personalized medicine mean that a healthy 65-year-old in 2026 has a 40% chance of reaching 95.

But here's the thing: Your private RRSP is a finite bucket. Your CPP is a Sovereign Pipeline.

- The Spend-Down Fear: Most retirees stop spending at 75 because they are afraid of running out of money. This "Frugality Trap" ruins the golden years.

- The Delayed Floor: When you have a maximized CPP (delayed to 70), you have the "Permission to Spend." You know that no matter what, the pipeline will keep flowing at its highest possible rate until your final breath.

6. The Survivor Benefit Trap: Protecting Your Partner

In the 2026 economy, dual-income masteries are common. But when one spouse dies, the "Survivor Benefit" calculation can be a shock.

The Math of the Cap: The total CPP you can receive as a survivor is capped at the maximum benefit for a single person. If both you and your spouse were already receiving the maximum, one benefit effectively disappears.

The Sovereignty Fix:

By delaying your own CPP to 70, you are increasing the "Base Amount" that the survivor calculation is pegged to. This maximizes the floor for the surviving partner, ensuring that the "widow's penalty" doesn't lead to a loss of sovereignty in their 80s.

7. Tactical Execution: The 2026 CPP Workflow

If you are 60-64 today, here is your forensic checklist to secure your sovereignty:

- Audit Your MSCA: Log into Service Canada. Do not look at the "Current" number; look at the "Age 70" projection.

- The "Bridge" Simulation: Stress test your private assets. Can you fund 10 years without CPP? If yes, the delay is mandatory.

- OAS Integration: Remember that Old Age Security (OAS) can also be delayed to 70 for a 36% increase. Combining maximized CPP + maximized OAS creates a "Sovereign fortress" that market volatility cannot breach.

- Tax Sensitivity: Drawing down your RRSP before 70 (while CPP is zero) is often more tax-efficient than waiting and being hit by the OAS clawback at 72.

8. Conclusion: The Sovereign Mindset

In 2026, the CPP is not a "government handout." It is a Tactical Financial Weapon. By intentionally delaying and building your "Sovereign Floor," you reclaim your life from the volatility of the markets and the whims of the central banks.

Master the math. Secure the floor. Rule your retirement.

SimRetire Tactical Intelligence: Forensic Insights for the 2026 Economy.

Ready to Run the Forensic Math?

Don't guess your breakeven point. Use our professional-grade simulator to find your specific "Point of Mastery."

Launch Forensic Engine